The most common resolution for a taxpayer facing an unpaid tax liability with the Internal Revenue Service (IRS) is an installment agreement. And yet despite the fact that it is the most widely used resolution, the installment agreement is still often mired in a debate between fact and fiction. Let’s get to the bottom of some of the IRS installment agreement options so we can guide taxpayers on the road to success.

Before getting into the details of IRS installment agreements, let’s make an important distinction about tax types. Individual income tax has the most flexibility when dealing with the IRS. Unpaid employment taxes, on the other hand, are heavily scrutinized by the IRS and more often have resolutions based on strict expense standards and a determination of ability to pay. In this discussion let’s focus on the individual and more standard opportunities.

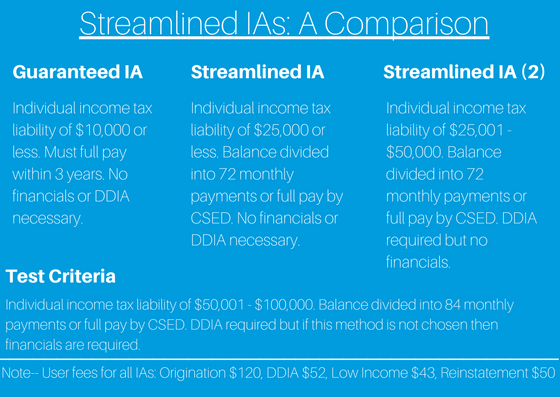

As I just noted some IRS installment agreements are based on ability to pay. Other, more routine agreements, are often referred to as streamlined because of the ease of processing involved in setting them up. These can be based strictly on the amount owed and set up over a defined period of time. Routine agreements are great considerations for taxpayers that are in compliance, have few complications and can afford to pay the predetermined amount.

Having the knowledge of the various types of basic IRS agreements is a great starting point for resolving a taxpayer’s unpaid liability. But, it’s just that, a starting point. The agreements should not be misconstrued as the taxpayers only alternative, rather a possible path of least resistance. And as straight forward as these agreements are, a practitioner eyeing the long term success of the agreement needs to consider much more. There are many considerations that should come in to play when thinking about whether to enter into a repayment plan with the IRS. Here are just a few thoughts to consider:

- Has a Notice of Federal Tax Lien already been filed against the taxpayer? This is typically done fairly early on the collection process. If it has not been done there is a good chance that the lien can be deferred by entering into a streamlined agreement.

- Can the taxpayer afford the amount that will be required by the agreement? If not, entering into a streamlined agreement will result in a default.

- Is an installment agreement the appropriate strategy based on the circumstances? Absent any pressure from the IRS, the taxpayer may be better served by going through other channels especially if there is a doubt as to whether the tax is really owed.

- Is the timing right? Imagine a scenario in which the taxpayer owes for 2014-2016. Before entering into an agreement for those years one must consider the implications of 2017 and 2018.

In the end, the mere existence and availability of these streamlined agreements does not mean they are the appropriate resolution to the tax liability. Although the IRS might prefer that a taxpayer simply walk in to one of the easy offerings it is important for a tax practitioner to evaluate the totality of the taxpayer’s circumstances to properly put together an effective, winning strategy.